Most homeowners who consider installing rooftop solar do the math twice. First, on the upfront cost of the asset, and second, on the solar panel tax benefits in India, they think will sweeten the deal. But the second calculation usually disappoints. That’s because the Income Tax Act in India does not offer a rebate or deduction in direct income tax for installing solar panels at home.

Most of the tax-saving sections you find on the web cite solar tax benefits for homeowners that either expired years ago or were designed for businesses, not salaried employees.

But there’s some good news, too. As a homeowner in India, you don’t need a solar panel tax deduction to make solar financially worthwhile. There are some true solar incentives in India that only homeowners receive.

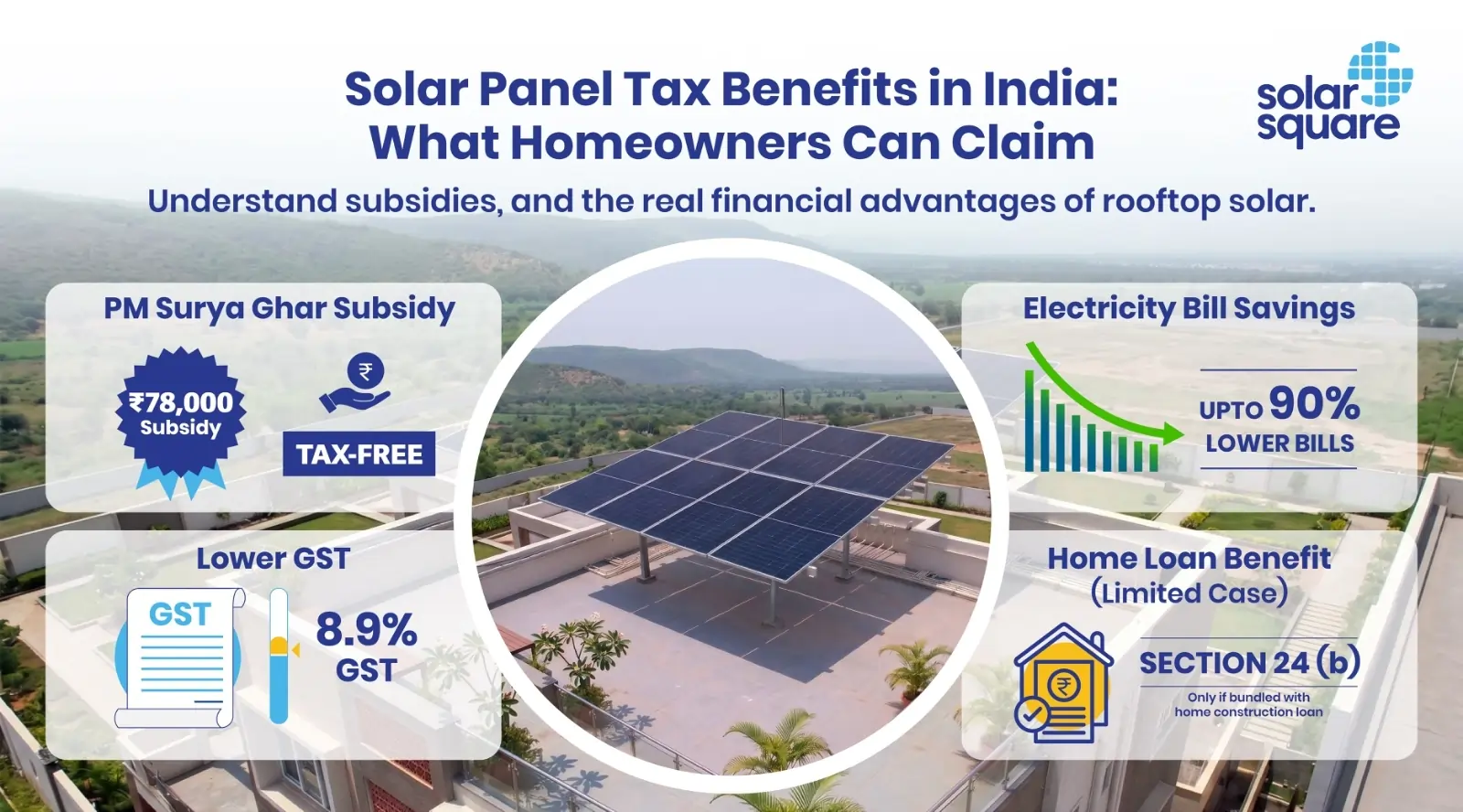

- The central government’s PM Surya Ghar Muft Bijli Yojana subsidy scheme offers financial support of up to Rs. 78,000 to homeowners installing systems of 3 kW or more. The best part? The subsidy amount you get is completely tax-free.

- The effective GST on residential solar installations is ~8.9%, much lower than the GST on most household electronics.

- The 25-year electricity bill savings on a well-designed rooftop solar panel system for homes run into the tens of lakhs of rupees, as your bills after going solar will get reduced by at least 90%.

This blog explains what solar tax benefits in India actually exist for homeowners, myths you shouldn’t pay heed to, and the solar incentives in India that make rooftop solar worthwhile.

The 4 Solar Financial Benefits for Indian Homeowners

Here’s an overview of the solar incentives in India that are available for homeowners:

- PM Surya Ghar Muft Bijli Yojana subsidy: This is a direct cash benefit of up to Rs. 78,000 from the central government for systems of 3 kW or more, credited to your bank account. This subsidy is fully tax-free and does not need to be declared as income in your ITR.

- State-level additional subsidies: Some states offer extra financial support on top of the central subsidy. Delhi and Uttar Pradesh, for instance, give homeowners an additional Rs. 10,000 to Rs. 30,000 depending on system capacity.

- Reduced GST on solar equipment: A residential rooftop solar installation attracts a GST of ~8.9%, unlike the higher 12-18% slabs that apply to electrical equipment.

- Solar loan interest: A solar loan, by itself, does not directly offer tax benefits on rooftop solar. But the monthly electricity bill savings exceed the EMI, which gives you an indirect cash flow benefit from day one.

Accelerated depreciation is a powerful tax-saving tool in India. However, it is available to businesses installing solar, not individual salaried homeowners. It helps businesses write off up to 40% of the asset’s value in the first year itself.

Are There Any Direct Solar Panel Tax Benefits in India for Homeowners?

The short answer is no. There is no standalone income tax deduction in the Income Tax Act, 1961, that you can claim simply because you bought and installed rooftop solar at home. No section lets a salaried homeowner subtract the cost of solar panels from their taxable income.

However, there is one narrow exception worth mentioning.

If your solar installation is bundled into a home construction loan, where the cost of solar is part of the total cost of constructing your house, then the loan interest qualifies for the standard home loan deduction. But be aware that this is not a solar-specific benefit. It is a home loan benefit where solar rides along because it was built into the construction cost.

For everyone else, the benefits come through indirect but financially significant routes.

- Government subsidy of up to Rs. 78,000, depending on the size of the solar system.

- Electricity bill savings, as a well-planned rooftop solar system can cut your monthly bills by 90% for at least 25 years.

Together, these create a return on investment that far exceeds what most income tax deductions can save.

Income Tax Benefits on Solar Panels Through Home Loans

Many banks market solar loans alongside home loans, blurring the distinction between the two.

- A solar installation can qualify under home loan tax deductions only if it is included in a home construction loan.

- If you are building a house and your home loan covers the cost of the structure plus the rooftop solar system as part of the construction package, the entire loan interest, including the portion for solar, falls under Section 24(b) deductions.

- A standalone solar loan from your bank, even if marketed under PM Surya Ghar Muft Bijli Yojana, does not qualify under Section 24(b).

- The same applies to a personal loan or a top-up loan taken specifically to fit solar on an existing house. These loans are for equipment, not for the home itself, and the Income Tax Act draws a clear line.

The deduction applies to the interest paid on the loan, not to the cost of the solar panels themselves. So, even in the eligible scenario, you are claiming home loan interest, not a solar deduction.

What About Sections 80EE and 80EEA?

These two sections are often brought up in solar tax discussions, but they do not apply to your solar installation.

- Sections 80EE and 80EEA were both designed for first-time homebuyers purchasing a residential property, not for installing equipment in a house.

- Section 80EE applies only to home loans sanctioned between 1 April 2016 and 31 March 2017.

- Section 80EEA covers affordable housing loans sanctioned between 1 April 2019 and 31 March 2022.

Both windows are closed for new loans.

If you took a qualifying home loan during those specific windows and are still repaying it, you can continue claiming the deduction until the loan is fully repaid. But neither section can be used to claim a deduction on a solar loan or on the cost of installing rooftop solar.

What About Section 80C?

Section 80C covers the principal repayment portion of a home loan. The same logic as above applies here.

- If solar is part of a home construction loan, the principal repayment qualifies under Section 80C along with the rest of the home loan principal.

- A standalone solar loan does not qualify because it is not classified as a housing loan in the eyes of the Income Tax Act.

Difference Between Solar Subsidy and Income Tax Benefits on Solar Panels

Many homeowners use the terms subsidy and tax benefits on solar panels interchangeably. But the two are very different, and understanding the difference is key to evaluating the real solar incentives in India that work for you.

| Benefit Type | Who Gets It | How it Works |

| PM Surya Ghar Subsidy | Homeowners with grid-tied rooftop solar systems. | It’s a 100% tax-free financial assistance of up to Rs. 78,000, depending on the system size installed, directly transferred to your bank account to make rooftop solar affordable. |

| Home loan tax deduction | Homeowners with solar bundled into a home construction loan. |

|

| Net metering savings | Residential and commercial consumers with bidirectional net meters. |

|

| Accelerated commercial depreciation | Businesses, MSMEs, and commercial entities |

|

Do Businesses Get Different Solar Tax Benefits?

Commercial entities can claim depreciation benefits under Section 32 of the Income Tax Act. It means they can write off 40% of the solar asset’s value in the first year, reducing their taxable income significantly.

For a business in the 30% tax bracket investing Rs. 10 lakh in solar, this translates to a tax saving of Rs. 1.2 lakh in year one alone.

- These solar tax benefits for homeowners are not available to salaried individuals installing rooftop solar.

- Accelerated depreciation requires the asset to be used for business purposes and the buyer to be a registered business entity.

Government Solar Incentives Available for Homeowners in India

While direct solar panel tax benefits in India are limited for homeowners, the government offers financial support through subsidies and solar power net metering. These are not tax deductions, but the value of the incentives reduces your cost of going solar far more than any tax provision would.

#1. PM Surya Ghar Muft Bijli Yojana

This is the central government’s financial help to homeowners installing grid-connected rooftop solar systems for personal use. It’s a direct cash benefit of up to Rs. 78,000 for systems of 3 kW or more.

The structure of the PM Surya Ghar subsidy is pretty straightforward:

- Subsidy for 1 kWp: Rs. 30,000

- Subsidy for 2 kWp: Rs. 60,000

- Subsidy for systems above 2 kW: Rs. 18,000 per kW, up to 3 kWp.

The maximum subsidy under the PM Surya Ghar Muft Bijli Yojana is capped at Rs. 78,000 for systems of 3 kWp or more.

This subsidy is a legitimate solar tax exemption in India that genuinely benefits homeowners, as you do not need to declare it as income on your ITR.

#2. State-level Solar Incentives and Net Metering Benefits

While in most states only the PM Surya Ghar Muft Bijli Yojana Subsidy is offered as a solar incentive in India, some states offer state subsidies on top of the PM Surya Ghar Muft Bijli Yojana subsidy to make rooftop solar even more attractive.

- Delhi state solar subsidy: The Delhi government offers a subsidy of Rs. 10,000 per kW, capped at Rs. 30,000 for systems of 3 kWp or more.

- Uttar Pradesh state solar subsidy: The UP government offers a subsidy of Rs. 30,000 for rooftop solar systems of 2 kWp or more.

- Assam state solar subsidy: The Assam government offers a state subsidy of Rs. 15,000 per kW, capped at Rs. 45,000 for solar systems with a capacity of 3 kW or higher.

- Chhattisgarh state solar subsidy: The Chhattisgarh state government offers a subsidy of Rs. 15,000 per kW, capped at Rs. 30,000, for systems with a capacity of 2 kWp or higher.

Is Income Earned Through Net Metering Taxable?

Net metering in India is not supposed to be treated as an additional income source in the literal sense. It’s more aligned with earning credits to lowering your electricity bills, resulting in massive savings from a rooftop solar system.

If the credits are even purchased by the DISCOM, it’s done at an extremely low tariff, making the financial returns negligible. Hence, upsizing solar with the motto of selling solar power to the DISCOM is not a great idea for homeowners.

Let’s understand how net metering works and what it’s used for:

- Residential net metering is not treated as business income: Most homeowners use solar for personal consumption, and the surplus exported is incidental. The Income Tax Act does not treat this as a commercial activity for a salaried individual.

- Direct cash payouts may require tax evaluation: A few states pay cash for residual export credits at year-end settlement. The amounts are small for residential users, but if you receive a cash payout, it is worth a quick conversation with your CA to confirm reporting requirements. The Chandigarh Joint Electricity Regulatory Commission (JERC) explicitly allows residential prosumers an annual cash payout for net excess credits at the Average Power Purchase Cost (APPC). In Delhi, excess solar generation can be carried forward, but consumers can opt for a cash payout at the end of the financial year if the surplus exceeds a certain threshold (dependent on local DISCOM policies)

- Bill adjustment credits are not taxable: When net metering simply reduces your monthly electricity bill, there is no taxable income event for a residential user. You are saving on a personal expense, not earning income.

- Rules vary by state and DISCOM: Net metering policies, settlement mechanisms, and cash-out rules differ across states. Always check your local DISCOM’s policy before assuming the tax treatment of your net metering credits.

Forecast your savings with solar on your investment on the SolarSquare’s plantCalculate your savings

![]()

Common Myths About Solar Panel Tax Benefits for Homeowners in India

Here are the most common myths about solar panel tax benefits for homeowners that you must know before making a financial investment that will remain on your rooftop for at least 25 years.

- Myth 1 – Buying rooftop solar automatically reduces your income tax: There is no standalone income tax deduction in the Income Tax Act for installing solar at home. Direct tax benefits exist for businesses in the form of accelerated depreciation, not for salaried homeowners.

- Myth 2 – Every solar loan qualifies for tax benefits: A standalone solar loan, even one taken under PM Surya Ghar Muft Bijli Yojana, does not qualify for Section 24(b) deductions. Only solar bundled into a home construction loan rides along on home loan tax benefits.

- Myth 3 – Government solar subsidy and tax deductions are the same thing: A subsidy is a direct cash credit that reduces your purchase cost. A tax deduction lowers your taxable income at filing time. The PM Surya Ghar Muft Bijli Yojana subsidy is far more financially valuable to a homeowner than any income tax benefits on solar panels.

- Myth 4 – Solar tax benefits are the main reason to install rooftop solar: For a homeowner, the real returns from solar come from the subsidy, the GST reduction, and 25 years of near-zero electricity bills. Tax savings, where they apply, are a small bonus.

Old Tax Regime vs New Tax Regime: Does It Affect Solar Benefits?

Most home loan tax deductions are available only under the old tax regime. Under the new tax regime, which is now the default for individuals, Section 24(b) interest deduction is not allowed for self-occupied property, and Section 80C principal repayment cannot be claimed either.

This makes the tax angle on home-loan-bundled solar effectively zero for most new tax regime filers.

The good news is that this changes very little of the actual financial picture for a solar homeowner. The biggest solar incentives in India for homeowners, the PM Surya Ghar subsidy and the reduced GST on solar equipment, do not depend on which tax regime you choose. You receive them as long as you meet the eligibility conditions set by the government.

Practical Tax Filing Checklist for Solar Homeowners

Once your rooftop solar is installed and running, here is a quick checklist to keep your tax filing clean and your records audit-ready.

- Do not declare the PM Surya Ghar Muft Bijli Yojana subsidy as income in your ITR: It is a government capital subsidy and qualifies as a tax-free solar tax exemption in India for homeowners.

- Retain the subsidy disbursement letter from the DISCOM: Keep it on file for records and any future verification.

- Keep your solar system invoice showing the GST charged: This serves as proof of your purchase and the applicable tax structure at ~8.9%.

- Do not claim solar loan interest under Section 24(b) for a standalone solar loan: It is not classified as a housing loan and does not qualify for the deduction.

- If self-employed or running a business, consult your CA on accelerated depreciation under Section 32: Solar installed for business use can qualify for 40% depreciation in year one.

- If GST-registered, evaluate Input Tax Credit on solar equipment GST paid: This is available for business installations and can further reduce your effective cost.

- If solar is bundled into a home construction loan, confirm with your bank and CA whether the interest qualifies under Section 24(b): Documentation must clearly show solar as part of the construction cost.

Conclusion

Solar panel tax benefits in India exist, but they look very different from what homeowners expect. There is no special section in the Income Tax Act that rewards you for installing rooftop solar at home. The main financial benefits come from the PM Surya Ghar Muft Bijli Yojana subsidy of up to Rs. 78,000 for systems of 3 kW or more, reduced GST on solar equipment, and 25 years of near-zero electricity bills.

- For homeowners with solar built into a home loan, the standard loan deductions under Section 24(b) and Section 80C continue to apply.

- For businesses, accelerated depreciation under Section 32 is one of the most powerful tax-saving tools in the country.

But for the average salaried homeowner installing solar on an existing house, the real return is in electricity bill savings, not in the tax return.

If you have been waiting on solar because you were unsure about the income tax benefits on solar panels, the better question to ask is how much you can save on your electricity bill over the next 25 years. For any further queries about installing rooftop solar at home, you can book a free solar consultation with SolarSquare today.

FAQs

Does the PM Surya Ghar Muft Bijli Yojana subsidy reduce taxable income?

The PM Surya Ghar subsidy does not directly reduce your taxable income, because it is not income to begin with. It is a tax-free government subsidy that reduces your upfront cost of installing rooftop solar. You do not need to declare it in your ITR.

Is solar subsidy taxable in India?

No, not at all. Solar subsidies, including the PM Surya Ghar Muft Bijli Yojana central subsidy and any additional state subsidies, are not taxable under the Income Tax Act, 1961. They are treated as government capital subsidies and do not need to be reported as income.

Can salaried employees claim solar tax benefits?

Salaried homeowners cannot claim a direct income tax deduction for buying solar. The main solar benefits for homeowners include the PM Surya Ghar Muft Bijli Yojana subsidy, reduced GST on solar equipment, and long-term savings on electricity bills.

Are solar loans eligible for Section 24 deductions?

A standalone solar loan, including one taken under PM Surya Ghar Muft Bijli Yojana is not eligible for Section 24(b) deductions. The deduction applies only when solar is included in a home loan, where the cost of solar is built into the overall loan.

Can I claim Section 80C on a solar loan?

You cannot claim Section 80C on a standalone solar loan. Section 80C covers principal repayment on a housing loan for the purchase or construction of a residential property. Only if solar is bundled into a home loan does the principal repayment qualify, along with the rest of the housing loan principal.

Does Section 80EE apply to solar panels?

No. Section 80EE is a first-time homebuyer benefit that applied only to home loans sanctioned between 1 April 2016 and 31 March 2017. It was meant for the purchase of residential property, not for installing solar panels. Existing borrowers from that window can continue claiming it until their loan is repaid, but it cannot be used for a solar panel tax deduction.

Can a housing society or RWA claim any tax benefits on solar installation?

Yes, housing societies and RWAs are registered legal entities that file their own income tax returns, and they can claim tax benefits available to them based on their income structure and registration type. They are also eligible for a separate PM Surya Ghar subsidy of Rs. 18,000 per kW (up to Rs. 90 lakh) for common-area solar installations. Since society tax treatment depends on the specific income sources and registration, it is best to consult a CA for the exact benefits applicable to your society.

Who can claim accelerated depreciation on solar panels in India?

Accelerated depreciation under Section 32 of the Income Tax Act is available to businesses, MSMEs, and commercial entities that install solar systems and use them for business purposes. They can claim 40% depreciation on the asset’s value in the first year. Individual salaried homeowners installing rooftop solar for personal use cannot claim this benefit.